You can deduct from their taxes the pension payments to your spouse or to another person that receives it on behalf of your spouse. This text covers the pensiones under the divorce decree or under a written agreement of separation which has taken place after 1984. Explains what is deductible in the case of spouses who pay the pension, and what is taxable, if it is you is who receives the pension.

Pension payments, under an instrument of separation, as it is a decree of divorce or a written agreement, are deductible if the following requirements are met:

- You and your spouse (ex-spouse) do not send a joint income tax return,

- You pay in cash (this includes checks and money orders),

- The instrument of divorce or separation does not specify that the payment is not a pension,

- If you and your spouse are legally separated under a decree of divorce or child support, separate, and you and your former spouse do not share the same household or residence;

- Has No liability to make any payment (in cash or testamentary) after the death of your spouse or former spouse; and

- If your payment is not for child support.

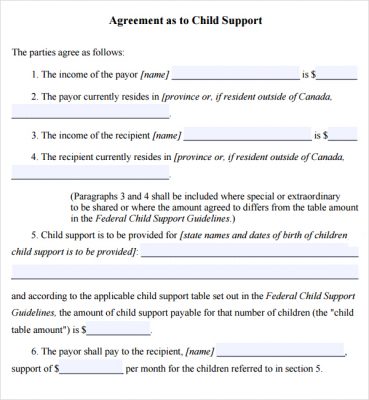

The maintenance of a child is never deductible. If your divorce decree (or some other written document) states that you must pay child support for a child and spousal support, and you pay less than the total required, the payments will be used first and foremost for the payment of child support. Any amount remaining will be considered for the board.

Agreements, probate, whether on payment of cash or deferred payments (even if it is required in the divorce decree, or other documents), do not qualify as alimony. Any payment that is not required in the divorce decree, does not qualify as a pension. You do not have to itemize deductions in order to claim pension payments. You can claim the deduction on line 34a of Form 1040. You must provide the social security number of the person who receives the payments. If you do not, you could pay a fine of $50 and request a deduction may be rejected.

If you are the spouse or former spouse who receives the pension, you must report this amount as income on line 11 of Form 1040. If you don’t give your social security number of the spouse who pays the alimony, you could pay a fine of $50 dollars.